Telco AI Outlook 2026: Will This Be the Year CSPs Unlock Real Revenue Scale?

Three years into meaningful Telco AI commercialization and CSPs have demonstrated that AI can deliver real value. Across the 240 CSP and hyperscaler-led initiatives we’ve tracked since 2023, the picture is consistent: activity is maturing and is dominated by enterprise and industrial use cases.

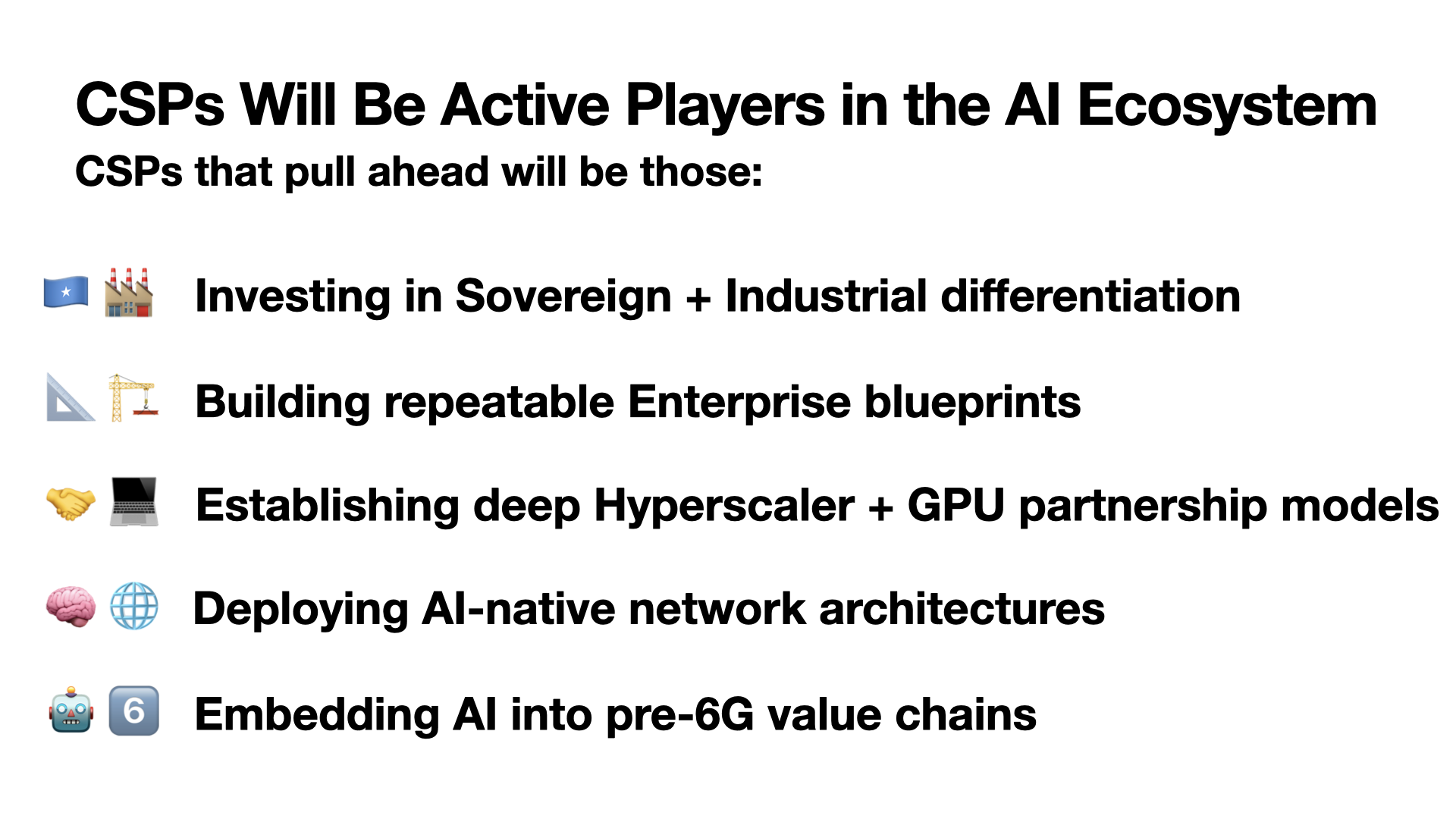

As 2026 begins, a pivotal question hangs over the industry: Will this be the year operators unlock repeatable, scalable monetization - or another cycle of incremental gains?

CSPs have invested aggressively in internal efficiencies (network automation, assurance, energy optimization) and customer-facing AI (CX agents, digital assistants). Yet it’s the enterprise domains - sovereign platforms, industrial AI, and vertical AI - that offer real margin potential, due to CSPs’ control of regulated data, edge infrastructure, and nation-scale networks.

Early leaders such as SK Telecom, Singtel, Deutsche Telekom, NTT Docomo, and e& are building foundations that rivals will struggle to replicate at speed, especially around sovereign AI stacks, industrial applications, and GPU-enabled edge architectures.

But operators can’t keep deferring scale: Telco AI will define AI‑native network economics, and falling behind risks missing the opportunities from the next wave of agentic, edge-driven innovation.

This 2026 outlook draws on high-level findings from the Telco AI Services & Impact Tracker - CSPs & Hyperscalers: Q3 2025, our paid dataset covering Tier‑1 AI service models, maturity, and ecosystem strategies. What follows is a free-to-air glimpse of the patterns we see shaping 2026.

Enterprise Domains Dominate Monetization - And the Gap Is Widening

Today, 60% of all monetized Telco AI services cluster around three proven domains:

Sovereign & Enterprise AI Platforms

Industrial & Vertical AI Services

Customer Experience & Virtual Assistants

Across the 15 Tier‑1 operators we track, 10 monetize more than half of their active AI portfolio. But the gulf between leaders (~70% monetization) and the rest (~39%) is widening - and that divergence will accelerate in 2026 as sovereign and industrial platforms scale.

Expect three shifts in 2026:

Sovereign platforms become the anchor of regulated AI activity and national AI strategies.

CSP + hyperscaler co‑built stacks (already 44% of initiatives) become the enterprise default.

Industrial replicability grows as private-network-led deployments prove multi-site repeatability.

The long-running “value-add” debate won’t vanish, but enterprises are already paying premiums for AI delivered with verified ROI, especially where compliance, performance, and integration matter.

Sovereign & Enterprise AI Platforms: The Regulatory and Technology Moat

2026 is shaping up to be the year sovereign AI moves from announcements to operational differentiation.

From our analysis of the 10 most significant deployments in 2025, three themes stand out:

South Korea

SK Telecom + NVIDIA Petasus AI Cloud

1,000+ Blackwell GPUs, 25× energy efficiency potential - positioning SKT as Korea’s national AI backbone.

Europe

Deutsche Telekom’s “AI Gigafactory” (with NVIDIA)

10,000 GPUs focused on industrial AI, EU sovereignty, and full-stack data-residency compliance.

Southeast Asia

Singtel Paragon GPUaaS

First regional Blackwell deployment; 30× faster LLM inference for sovereign enterprise workloads.

Looking ahead to 2026:

The Gigafactory, when live, will be a major landmark for EU-compliant industrial AI.

South Korea’s AI Basic Act (effective January 2026) will accelerate sovereign platform adoption.

3–5 major platform expansions are likely among early leaders, particularly in South Korea/ Japan.

A potential tipping point emerges if NTT Docomo’s GPU‑accelerated 5G network (first worldwide) scales as expected.

Sovereign AI is increasingly the most defensible strategic position CSPs can take: a convergence of regulated infrastructure, trusted data, and national AI ambitions.

Industrial & Vertical AI: The True “Techco” Differentiation Play

Industrial AI is where Telco AI becomes scalable, not just experimental. Our data shows:

72% of vertical AI deals involve partners and include 5G private/campus networks

GenAI (52%) and computer vision (32%) will increasingly become sought after capabilities

Signals heading into 2026:

Deutsche Telekom + Microsoft: Agentic AI for Industry 4.0 - robotics + video analytics demonstrating sub‑12‑month ROI

Telefónica + Etiqmedia: Vision-based logistics AI operating over 5.5G/NWDAF

T-Mobile + major US-based sporting events; Verizon + NVIDIA: AI media automation over private 5G for events and live production

Expect in 2026:

Growth in sustainability-linked industrial AI (energy, decarbonization, agriculture).

Asia as bellwether:

China’s “AI+ industry” initiative

Japan’s smart-city and mobility frameworks

Korea’s new oversight laws

Multi-site replication will become the norm for industrial deployments.

Industrial AI is emerging as the primary external revenue engine for CSPs - especially when paired with private 5G, slicing, and GPU-edge infrastructure.

Internal AI: The Profit Engine CSPs Cannot Ignore

AI now appears in 80% of CSP-internal initiatives, with 58% focused on:

network automation

autonomous assurance

energy efficiency

sovereign platform readiness

Key signals:

NTT Docomo + NVIDIA/Wind River: GPU‑accelerated 5G reducing power consumption by ~50% and TCO by ~30% - a potential industry blueprint.

Hyperscalers focusing ~62% of their telco AI activity on network/ops automation - accelerating CSP transformation pathways.

Expect in 2026:

Rapid adoption of energy optimization agents, potentially reducing opex 10–20% for leaders.

A shift toward GPU + edge inference architectures, enabling AI-native network patterns.

Internal AI becoming the economic base that funds enterprise AI expansion.

Consumer AI: Marginal Gains, Gradual Evolution

Consumer AI remains <4% of monetized activity. It is evolving, but not at a pace that shifts short-term revenue curves.

Signals for 2026:

Continued uptake of multimodal CX/chatbot agents.

Traction for AI-enhanced propositions (gaming, security, digital life).

Regulatory frameworks - particularly in China and the EU - shaping the pace and structure of AI adoption.

Consumer AI will matter long-term, but 2026 remains an enterprise-first Telco AI cycle.

Funding & Economics: Where the Money Actually Comes From

A major concern for CSPs is how to fund Telco AI while capex remains tight and returns nascent. The answer - based on what we’re seeing in Tier-1 portfolios - is clear:

1. Opex Savings Power the Next Wave

Internal AI is designed to self-fund growth. Around 58% of CSP-targeted initiatives focus on network automation + energy efficiency, and agentic/GenAI capabilities make up about two‑thirds of all internal activity. These savings will increasingly justify expansion into sovereign and industrial platforms.

2. Real Proof That the Model Works

NTT Docomo’s GPU-accelerated 5G deployment demonstrates the order of magnitude: ~50% lower power, ~30% lower TCO in core network functions. This level of economics is precisely what CSPs need to unlock the next phase of investment.

3. Hyperscaler Co-investment Reduces Upfront Burden

Hyperscalers now direct ~61–62% of their telco AI activity toward RAN/ops automation and infra, enabling opex-based scaling and co-build approaches - without jeopardizing CSP control of enterprise revenue.

4. Monetized Enterprise Domains Replenish the Pool

More than 60% of monetized Telco AI sits in regulated or industrial categories that produce recurring, defensible revenue - creating recurring cycles, not one-off spends.

Bottom line: Telco AI will be funded by automation, energy savings, partner economics, and enterprise revenue in the three dominant domains.

So 2026 is about compounding savings + targeted growth bets - not “big bang” investment.

2026: Still Modest Revenue - But the Right Foundations for AI-Native Networks

Our assessment: 2026 will not be the breakout year for Telco AI revenues. But it will be the year where foundations harden, playbooks clarify, and leaders consolidate strategic advantage.

© xWave Research, 2026

These leaders already show that defensible, recurring enterprise AI revenue is far more valuable than short-lived experiments - and their portfolios point clearly to where growth will concentrate as we approach 2027–2030.

Want the Full Playbook?

The Telco AI Services & Impact Tracker - CSPs & Hyperscalers includes:

Revenue impact ratings for 20+ AI service archetypes

Benchmarks across 15 Tier‑1 CSPs + hyperscalers

Detailed analysis of Telco AI initiatives starting Q1 2023.

Bi-annual updates tracking market shifts

If you need visibility into the categories, partners, and technologies shaping the next 18 months of Telco AI - the full dataset is available now.