5G Monetization Outlook 2026: Will This Be the Year CSPs Finally Crack the Scale Conundrum?

Four or more years into real 5G service commercialization and CSPs have proved 5G can deliver value - but not yet in the volumes once promised. We’ve tracked over 115 commercial initiatives since 2023 and the data is clear: the market has matured beyond hype, but uptake remains stubbornly limited. Revenues are real but modest, often in the low-single-digit millions per deal, and remain concentrated in enterprise niches.

As 2026 begins, the industry faces a pivotal question: Will this be the year operators finally unlock repeatable, scalable 5G service monetization - or another year of incremental but modest gains?

The enabling technologies are no longer the constraint. 5G SA, slicing, AI‑driven assurance, mmWave uplink, and now RedCap are all commercially ready. The real bottleneck - and the real opportunity - is turning these capabilities into services and business models that deliver outcomes enterprises - and consumers - care about. In 2026, the clearest traction points are already visible: differentiated QoS and AI‑powered network intelligence.

Industry forecasts point to accelerating enterprise demand, with private 5G networks alone projected to hit $5-17B globally by 2028-2030. Early leaders like Verizon, Deutsche Telekom, and T-Mobile are building irreplaceable expertise today, but CSPs can't keep deferring scale around services - 5G is the foundation for 6G, and kicking the can down the road risks leaving them unprepared for the next wave of AI-driven, immersive applications by 2030.

To inform this outlook, we're drawing on our latest Global 5G Services & Impact Tracker: Q3 2025 - a comprehensive dataset benchmarking Tier-1 CSP activity, revenue maturity, and ecosystem strategies. Available now as a paid service with bi-annual updates, it equips vendors, enterprises, and operators with actionable insights to navigate what's next. Here's a teaser of key trends shaping 2026, blending our data with fresh signals we’ve identified from market activity.

Enterprise Domains Dominate Monetization-And the Gap Could Widen

Over 80% of monetized 5G services cluster in three proven areas:

Private / Campus 5G

Live Events & Venues

Enterprise slicing & QoS-on-Demand

Across Tier‑1s, 13 of the 15 operators we track monetize more than half their active service portfolio, yet the gap between the top and bottom performers is widening. Leaders operate at ~82% monetization, while the rest remain around ~34%.

In 2026, expect:

CSPs to double down on enterprise-targeted slicing, which already accounts for 82% of slicing initiatives.

Bundles that combine QoS + security + AI analytics to become the next evolution, especially in industrial and logistics verticals.

A shift toward multi‑site, scalable enterprise services as proof points accumulate.

2026 won’t settle the ‘value‑add’ debate, but early signals already show enterprises paying premiums when slicing is delivered with predictive performance and AI‑assured reliability.

2. Private/Campus 5G: Moving From ‘Pilots Everywhere’ to Clear Differentiation

2026 is shaping up to be the year private 5G actually differentiates, not just deploys.

From our analysis of the 10 most significant deployments in 2025, a few themes stand out:

Germany: Deutsche Telekom + TRUMPF’s omlox-enabled micro‑location service is delivering sub‑12‑month ROI, thanks to precise manufacturing automation.

Spain/Germany: Telefónica’s 5G SA + computer vision rollout with Würth demonstrates how private 5G becomes a logistics optimizer - not just a connectivity enabler.

UK: Verizon’s multi‑site automation at Thames Freeport shows how CSPs are moving beyond one‑off projects in their home markets toward repeatable blueprints globally.

Expect 2026 to bring:

3–5 landmark multi‑site private 5G deployments per leading Tier‑1 operator.

A rise in sustainability‑linked 5G use cases, following examples like Orange supporting ArcelorMittal’s decarbonization.

Stronger integration between private 5G, digital twins, and ML-driven operations.

This domain remains the most likely bridge to meaningful revenue uplift - and at the same time the strongest precursor to AI‑native 6G architectures.

3. Live Events & Venues: The 2026 FIFA World Cup Will Be 5G’s Largest Stage Yet

Live events continue to be CSPs’ innovation sandbox. This is the kind of environment where slicing and uplink engineering are stress-tested in ways everyday usage rarely allows.

Our data shows:

73% of venue deployments rely heavily on slicing, typically for live video production or guaranteed uplink capacity.

The 2026 FIFA World Cup - spanning Canada, the US, and Mexico - is set to become the biggest real-world stress test of 5G capabilities since launch.

Expect:

Fan-facing XR overlays, including penalty‑view AR and real-time player analytics.

8K streaming and multi-view feeds, enabled by dense mmWave uplinks.

Advanced media production workflows using slicing and drone-mounted video systems.

Revenue here will remain modest in 2026 - but the exposure and learnings will be priceless. These deployments form the blueprint for the 2027–2028 period, when XR devices begin reaching mainstream affordability.

4. Consumer 5G: RedCap Potential Breakout?

Consumer monetization remains marginal, mostly tied to enhanced event experiences, but 2026 could see a lift from 5G RedCap.

Signals heading into 2026:

AT&T completed its RedCap-ready nationwide rollout in mid‑2025 (200M POPs).

e& has built foundational slicing capabilities for RedCap IoT/wearables.

Ecosystem support is emerging: Franklin Wireless’ RG350 hotspot and early wearables are now certified, paving the way for broader vendor launches.

What we expect in 2026:

A measurable uptick in mid-tier IoT/wearables connecting via RedCap.

No “explosion” - ecosystem maturity is still uneven - but a foundation for ARPU uplift over 2027–2028.

New consumer propositions around AI-enhanced security, gaming QoS, and family safety.

Whether RedCap becomes a breakout or a slow burn will depend on whether OEMs deliver enough devices at the right price points more than it will on network capability.

5. AI as the Margin Accelerator: From Internal Tool to Customer Differentiator

AI appears in 30% of monetized services tracked in our dataset - and this is just the beginning.

The shift in 2026:

From AI as an internal automation tool…

…To AI as a marketed feature baked into B2B services.

Examples include:

Predictive QoS packages inside slicing bundles.

AI-driven computer vision for logistics, retail, or security embedded within private 5G offers.

Network-core intelligence from vendors such as Ericsson and Nokia enabling AI‑orchestrated assurance.

Telco AI isn't just cost-saving-it's the bridge to premium revenue streams. By year-end, we expect at least six Tier‑1 CSPs to have productized AI as part of their B2B value proposition - laying the groundwork for 6G’s intelligent network fabric.

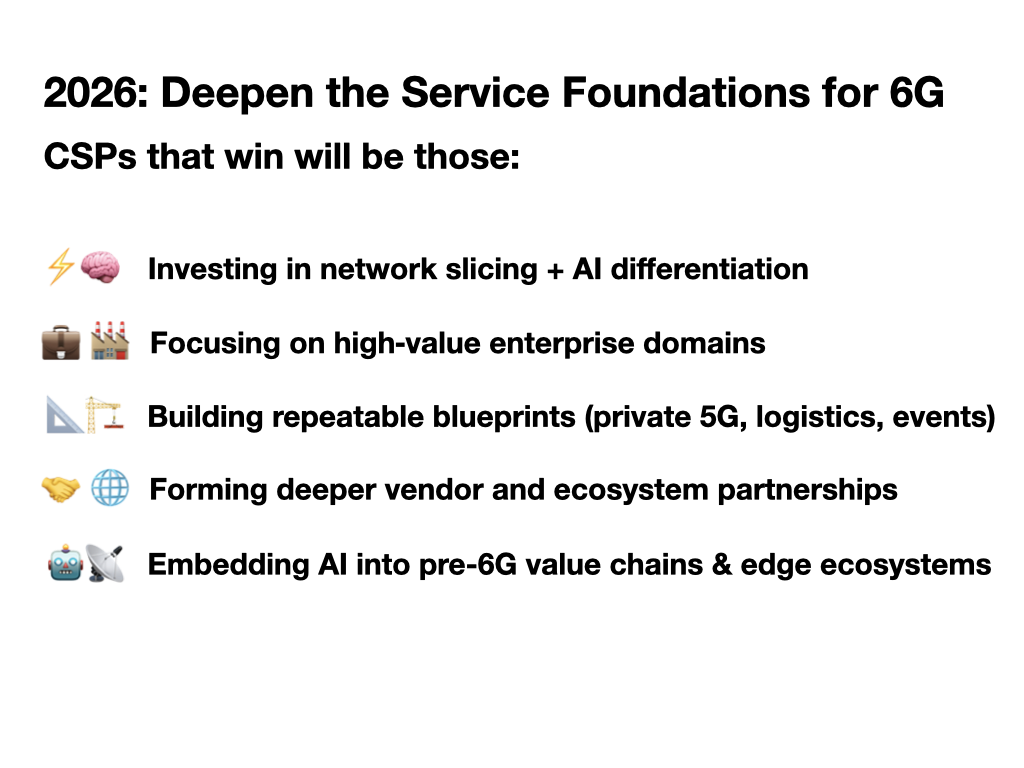

2026: Still Modest Revenue-but the Right Foundations for 6G

Our assessment: 2026 will not deliver a major step-change in 5G revenue scale, but it will deepen and validate the service foundations CSPs need for the 6G era.

© xWave Research 2026

These leaders are already demonstrating that steady, defensible revenue beats flashy, short-lived bets and limited trials - and their portfolios are a preview of where growth will concentrate as demand ramps toward 2027–2030.

Want the Full Playbook?

The Global 5G Services & Impact Tracker delivers:

Revenue impact ratings for 30+ service archetypes

Benchmarks across 15 Tier‑1 CSPs

Deployment and partnership models

Maturity scoring & competitive heatmaps

Bi‑annual updates tracking the shifts as they happen

If you need early visibility into the service categories, partners, and technologies that will define the next 18 months, explore the full dataset here.